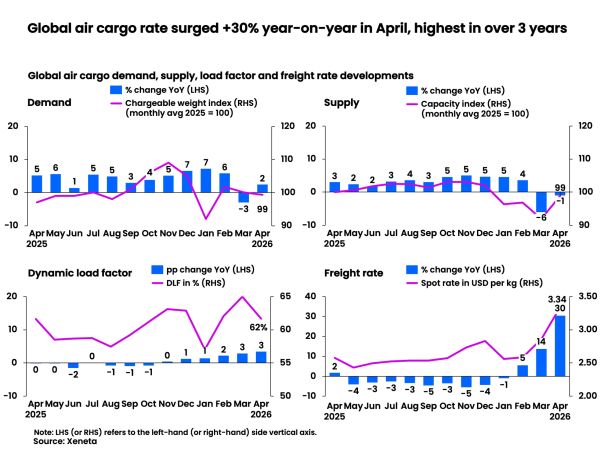

Global air cargo spot rates surged 30% year-on-year in April to $3.34 per kg to reach their highest level since October 2022, but the worst may be over for shippers as capacity returns on routes most affected by the Middle East conflict, and market fundamentals start to regain control of air freight pricing, according to industry analysts Xeneta.

April’s spot rate levels, which also included a +18% jump in long-term rates (valid for over one month) stirred uncomfortable memories of the pandemic era for shippers, when supply chains buckled under capacity shortages and freight costs soared to eye-watering levels.

Yet the parallel has its limits. Unlike the Covid shock, which upended global capacity wholesale, the most recent constraints are largely regional. More troubling, perhaps, is the fuel picture: crack spreads – the margin between crude oil and refined jet fuel – have now exceeded the peaks recorded during the pandemic, adding a cost burden that carriers cannot easily absorb or ignore.

But, Xeneta’s chief airfreight officer, Niall van de Wouw, says: “The worst may be behind us’ as rate increases show signs of easing, even on corridors most impacted by the conflict. This is all logical because the spike in airfreight rates was driven by a supply issue from the start. Now capacity is coming back, rates will come down, but not as quickly as they went up. Ultimately, market fundamentals will prevail.”

This will be welcome news for shippers who have been postponing Q3 and Q4 tenders with freight forwarders and ‘buying time,’ as they wait for the market to normalise, van de Wouw added.

Giving some cause for cautious optimism for these shippers, he said: “Global cargo capacity has largely recovered to pre-shock levels, and the jet fuel shortage, though reportedly spreading, has yet to grip long-haul intercontinental routes at scale. If those conditions hold, spot rates should ease in the weeks ahead and deliver some reprieve for shippers who have grown accustomed to unwelcome surprises.”

As shippers focus on acquiring the capacity they need for the second half of the year at a fair and equitable price, he advises them to gain a better understanding of how freight forwarders are moving their goods, and to be cautious of the so-called ‘feast of surcharges’ being touted around the market, led by surging jet fuel prices.

The jet fuel myth

“We need to bust the myth that if jet fuel goes up, airfreight prices (need to) go up. Fuel costs have gone up dramatically, but rates are starting to go down in specific markets.

“Recent developments regarding Transatlantic prices are a case in point. These rates have declined in recent weeks, despite the jump in jet fuel prices. The all-in cost a freight forwarder pays an airline is more driven by demand and supply than it is by fuel costs. We’ve been advising shippers not to have a fuel charge in their pricing mechanism, even though we hear that many surcharges are negotiable,” he said.

He also believes fears of fuel shortages forcing airlines to reduce flight schedules will not have a significant effect on airfreight.

Van de Wouw added: “In terms of the big trade flows, airfreight is mostly intercontinental, and these will be the last flights airlines will cut. Domestic or regional flying might be trimmed on marginal routes or flights merged so they’re fuller of passengers, but if it comes to a point where airlines are cancelling intercontinental flights because of a lack of fuel, then we have a bigger problem than just a lack of jet fuel.”

Shippers can limit the impact of higher costs by knowing more about how their forwarders are acquiring capacity, van de Wouw said. “You can’t always avoid higher rates, but the more you understand how your freight forwarder moves your stuff – like whether they are doing longer-term deals or buying capacity on the short-term market – the better you’ll be able to negotiate the financial impact it will have.

“Otherwise, you become more vulnerable to market disruptions, and you have a weaker starting point when you need to negotiate potential charges in your contract.”

The Middle East conflict continued to distort air freight rates across major corridors in April, with war-adjacent routes bearing the heaviest burden. Europe to Middle East spot rates hit a new high of $3.60 per kg in the week ending 26 April, up +108% on pre-conflict levels – the largest increase of any corridor. South Asia routes told a similar story: comparative rates to the Middle East and Europe doubled to $2.97 and $4.39 per kg respectively, while rates to North America rose +70% to $6.94 per kg.

Tentative signs of rates relief

There are tentative signs of relief, however. South Asia rates appear to have peaked in the week ending 12 April and edged down by single digits in the final week of April.

Southeast Asia corridors have followed, if less dramatically. Spot rates to the Middle East and Europe rose +43% and +61% from the pre-Iran conflict levels to $3.78 and $5.12 per kg respectively, while rates to North America climbed +33% to $6.46 per kg. Europe and North America-bound rates from the region now appear to be plateauing, though Middle East rates have yet to stabilise.

Northeast Asia lagged its neighbours. Outbound rates to the Middle East, Europe, and North America reached new highs of $5.25, $5.63, and $5.54 per kg respectively in the week ending 26 April – yet percentage increases remained modest compared with South and Southeast Asia. The lag likely reflects the delayed pass-through of jet fuel surcharges, which track actual fuel price movements with a delay; spot fuel prices themselves peaked in early April.

As highlighted by van de Wouw, the transatlantic corridor stands apart. Europe to North America rates fell -17% to $2.57 per kg, the only major corridor to record a decline. The divergence is instructive: air freight pricing responds to supply and demand, not costs. Despite rising jet fuel prices, airlines switching to summer schedules have flooded the corridor with additional passenger belly capacity, pushing cargo load factors down ten percentage points month-on-month and dragging rates with them.

But even with a +2% growth in demand in April, the challenges facing airlines, forwarders, and shippers will not end once the Middle East situation calms.

What happens next to demand?

“The big question is what will be left in terms of demand after all the inflationary pressure, all the uncertainty, and all the tremendous increases in fuel and production costs ease? What will it mean for Q3 and Q4 because everything that has happened in the last few weeks was against a backdrop of a not-too-rosy outlook for 2026,” he said.

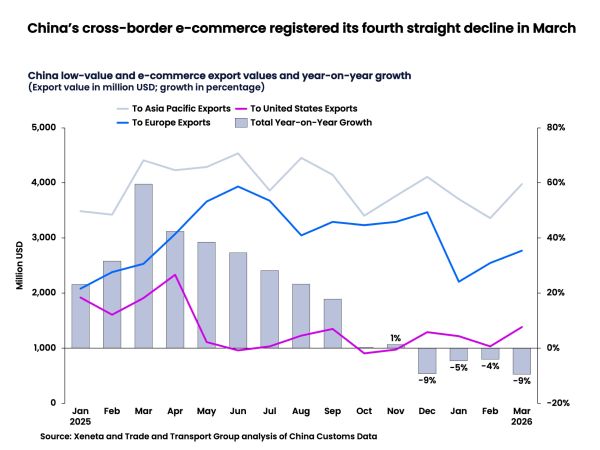

A -9% year-on-year drop in e-commerce shipment volumes ex-China in March, based on China Customs’ latest data, will add to concerns. While some of this volume may have shifted into air freight consolidations, and, therefore, be excluded from this data, van de Wouw believes the downward trend seen over the last 4 months ex-China indicates that, for air freight demand, “the B2C e-commerce growth seems to be over”.

While Xeneta has previously highlighted the resilience and maturity of airline, forwarder, and shipper relationships, the expected rebalancing of rates in the coming weeks and months is also being driven by a greater understanding of market conditions.

Van de Wouw commented: “I was taking part in a roundtable discussion two weeks ago and referenced the level of maturity in the market. One shipper acknowledged my comments but said “we look at it differently”, and added that the increased transparency in the market from companies like Xeneta means there is less “wriggle room” for higher prices, which is benefitting shippers.

“Overall, we do think we have seen the peak for global air freight rates, and we expect them to go down on more lanes, but, based on recent experience, there will undoubtedly be an underlying concern about what’s next in terms of trade disruption.”