The game of ‘cat and mouse’ between some of the world’s biggest trading nations may have taken its first nibble at international e-commerce volumes in February’s global air cargo market data with spot rates from Shanghai to the US dropping -29% month-on-month to US$3.23 per kg, according to the latest industry analysis by Xeneta.

Even allowing for the earlier Lunar New Year and the seasonal e-commerce slowdown at the start of the year, the fall in Shanghai-US spot rates, following the US’ temporary removal of the de minimis exemption on Chinese shipments, may be one of the first indicators that “the regulatory and political conversations are starting to affect the air cargo market,” said Xeneta’s chief airfreight officer, Niall van de Wouw.

He explained: “When the e-commerce boom took off, it very quickly clogged up the Hong Kong and southern China market because of so much outbound demand. So, the e-commerce market started to venture eastwards to Shanghai, even though it was less desirable due to additional cost.

“If a fall in e-commerce volumes means there’s currently more available capacity to do business out of Hong Kong and southern China again, we would expect Shanghai to be the first market to feel this impact, and that’s what we saw in February. This may be short-term, but the uncertainty around e-commerce is impacting the market.”

In comparison, the Shanghai-to-Europe spot rate saw only a modest -2% month-on-month decline to $3.86 per kg.

Overall, global air cargo demand grew by +4% year-on-year in February, marking a continued slowdown from the double-digit growth seen in every month of 2024. By calibrating the earlier Lunar New Year this year, the combined air cargo demand for January and February rose by a modest +3% compared to the previous year.

In addition to the US de minimis change, other factors likely influencing the monthly performance included a high comparison base in 2024 and the diminishing impact of Red Sea disruptions on air cargo volumes, as supply chains continued to adapt to longer transit times.

Global air cargo capacity supply in February also stayed flat compared to a year ago. The combined January and February capacity edged up by just +1%, while the dynamic load factor for the first two months of 2025 remained unchanged from a year ago at 59% in February. Dynamic load factor is Xeneta’s measurement of capacity utilisation based on volume and weight of cargo flown alongside available capacity.

The global air cargo spot rate (valid for up to one month) in February increased at its slowest pace year-on-year since June 2024, rising by +10% to $2.53 per kg. In contrast, the global seasonal rate (valid for longer than one month) dropped -1% year-on-year to $2.21 per kg, reflecting the market’s changing supply/demand dynamics.

In terms of month-on-month development, the global air cargo spot rate declined -5%.

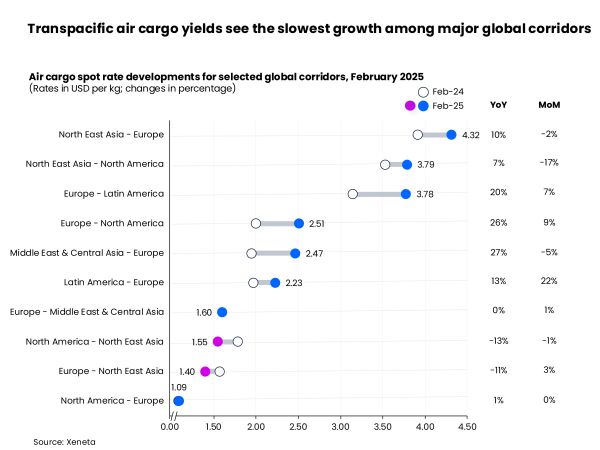

Among the major global corridors, the Northeast Asia to Europe market saw a +10% increase versus a year ago, to $4.32 per kg, but fell -2% month-on-month, while Northeast Asia to North America spot rates experienced the steepest month-on-month decline, dropping -17% to $3.79 per kg.

Meanwhile, the Transatlantic market remained buoyant. Spot rates from Europe to both Latin America and North America recorded high single-digit growth month-on-month, maintaining levels over +20% higher than a year ago. This elevated spot rate reflects limited passenger belly capacity during the winter flying season as well as freighter capacity shifting away from the corridor.

On the other hand, ample backhaul capacity led to the largest spot rate declines in both the North America and Europe to Northeast Asia markets, both registering year-on-year falls exceeding -10%.

Heading into 2025, Xeneta was forecasting a year of +4-6% growth in the global air cargo market, after its strong performance in 2024. Growing trade tension since then now place a big question mark over the outlook.

“With general cargo demand in the doldrums in recent years, the surge in e-commerce has been the saviour of the air cargo market performance. If this now takes a significant hit, if that happens, it will have a profound effect on airfreight rates around the world,” van de Wouw said.

For now, the big e-commerce players and general cargo shippers are buying time instead of cargo capacity to avoid commitments which might bring added financial risk.

“From the conversations we are hearing, some shippers are clearly looking for ways to minimise the impact of US tariffs, while others will be anticipating lower airfreight rates if e-commerce volumes show a sustained dip.”

This is also going to have a knock-on impact on other markets, van de Wouw said, adding: “If I was shipping ex Vietnam to the US right now, for example, I’d be concerned about the impact on rates if more shippers descend on this corridor to lessen the impact caused by tariffs on direct shipments from China to the US,” he added.

Further complicating the matter are proposed US port fees for Chinese built ships, which could throw ocean schedules into disarray, in the short-term driving up container freight rates and even prompting a shift from sea to air.

What’s next? Uncertainty and trade tension

The tariffs imposed by the Trump administration in the US and the awaited international response are causing increasing ripple effects across the global air cargo market, prompting strategic adjustments from key stakeholders.

With upcoming summer schedule changes and ongoing trade tensions, airlines are currently reassessing their freighter capacity strategies. Many may opt to shift routes toward Southeast Asia rather than China or reposition capacity to the Transatlantic.

Uncertainty in the market has led to freight forwarders delaying their block space agreement negotiations with airlines as they await more clarity on demand and pricing.

Meanwhile, some shippers are postponing annual contract negotiations from Q2 2025 while opting for shorter-term agreements in the first half of the year.

Van de Wouw says it’s a hard market to call: “This is a situation completely outside of the control of the air cargo market and there’s a great deal of noise, which is adding to stakeholders’ anxiety. The issue is no one knows what the end game is and what’s going to happen from a regulatory perspective, and how this will impact consumer confidence.”