July’s Crowdstrike IT outage produced no significant ongoing disruption to resurgent air cargo demand, with rates rising for a sixth consecutive month, says market analyst Xeneta.

Global average air cargo spot rates reached US$2.66 per kg in July, 20% higher year-on-year. This was again driven by strong global cargo demand growth. July volumes rose +13% year-on-year, thanks to buoyant e-commerce demand from Asia as well as the comparatively low demand base in the corresponding month in 2023. In contrast, global air cargo supply grew at only 2% year-on-year this July.

Demand growth alongside only a modest increase in capacity supply produced an expected boost to the global dynamic load factor. It exceeded last year’s level by five percentage points, reaching 59% in July.

With summer holidays starting in July, global air cargo demand slowed month-on-month. This was echoed by the ocean container shipping market, where container spaces in recent weeks became easier to book and spot rates on the major fronthaul trades from the Far East to Europe and the US either declined or flattened.

The global IT outage affecting Microsoft systems on 19 July brought widespread disruption, with flight delays and cancellations that lasted more than a week. The resulting cargo backlogs saw cargo load factors on some impacted airlines increase up to 4 percentage points compared to the previous week. But load factors had mostly recovered to pre-outage levels by 28 July.

As is often the case, short-term panic among shippers and forwarders pushed up the price of capacity, which rose to its highest level of the year in the last week of July to a global average air cargo spot rate of $2.70 per kg.

Looking ahead to the remainder of 2024

Strong year-on-year growth in air cargo demand is expected to extend into August and September, in part due to the low base set last year.

Heading to the second half of the year, disruptions in the Red Sea will likely continue to pose risks to supply chains due to container vessels’ longer sailing times and reduced schedule reliability. Despite the container market’s early peak season, the current situation may last until China’s Golden Week in October.

On top of this, potential sea port strikes in Hamburg and the US East and Gulf Coasts could coincide with the much-anticipated peak season for airfreight and apply further upward pressure on air cargo rates, as Xeneta highlighted last month.

Xeneta chief airfreight officer, Niall van de Wouw, said: “For the air cargo market, it’s now all eyes on late August for the first signs of a proper peak season, which would be the cherry on top of the cake for airlines after such unexpected volumes and demand growth in the first seven months of the year.

“In July, had the IT outage taken longer to fix, we might have seen a slightly different outcome. However, once again, air cargo showed resilience, after seeming to have dodged another major disruption. Going into the peak time of the year, airlines might just be starting to think their tailwinds will hold out.”

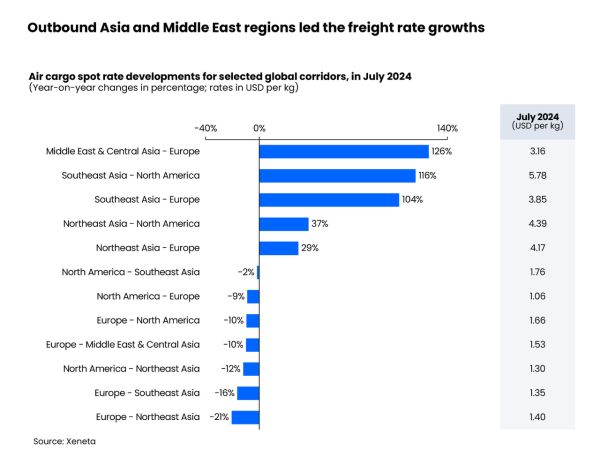

Middle East and Central Asia to Europe continued to lead year-on-year growth in regional cargo spot rates in July. Its July average spot rate surged 126% year-on-year to $3.16 per kg. Ongoing Red Sea disruptions have helped to keep air cargo rates high, while recent unrest in Bangladesh, which led to port and airport backlogs that will take weeks to clear, could further raise cargo rates in the coming weeks.

Outbound Southeast Asia to North America and Europe lanes took second and third places in terms of growth. Surging cargo demand more than doubled cargo spot rates from a year ago to $5.78 per kg and $3.85 per kg respectively.

These lanes were followed by outbound Northeast Asia markets, supported by strong e-commerce demand and general cargo volumes recovery.

Cargo spot rates to North America and Europe grew around 30% year-on-year to $4.39 per kg and $4.17 per kg, partly due to a high base last year.

As expected, backhaul trades on the above-mentioned lanes and transatlantic trades experienced year-on-year declines in spot rates. This was due to adequate capacity on the return leg and increased belly capacity on passenger flights to meet summer holiday season demand.