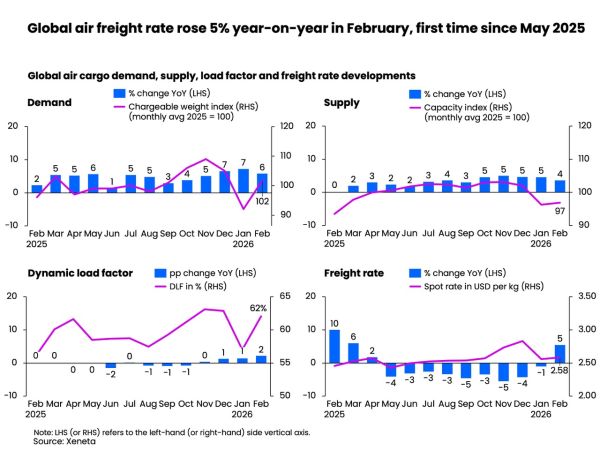

Another rise in air cargo market demand in February 2026, up +6% year-on-year, continued the encouraging spike in volume seen over the previous two months, and signalled underlying market resilience, despite the level of global trade and economic turbulence experienced over the past year.

But, five days into March, and with conflict now escalating in the Middle East, the market outlook is, once again, open to question, says industry analyst Xeneta.

Demand growth last month continued to exceed available capacity growth of +4% year-on-year, boosting dynamic load factor two percentage points higher to 62%. Dynamic load factor is Xeneta’s measurement of capacity utilisation based on volume and weight of cargo flown alongside available capacity.

Boosted by a mini peak season rush ahead of the Lunar New Year, air cargo spot rates recorded their first monthly increase since May 2025, up +5% to US$2.58 per kg. As well as Lunar New Year, this increase was supported by the continued depreciation of the US dollar compared to a year ago.

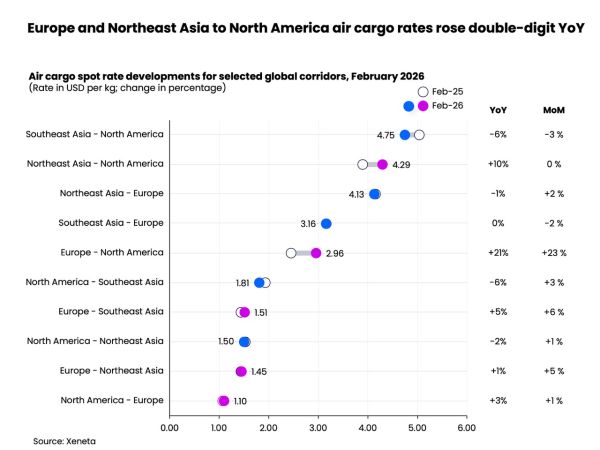

At a corridor level, Europe-North America saw the biggest year-on-year increase in air cargo spot rates in February of +21%, while demand for semiconductors continued to invigorate Northeast Asia-North America rates. It was the only other corridor to see double-digit growth of +10% in February, compared to a year ago.

Tariff impacts, however, weakened China to US air cargo demand, while China to Europe volumes remained relatively stable, but neither corridor repeated the typical pre-holiday cargo rush at the start of 2025. This hints at what’s likely to happen in 2026. Some Asia-based airlines with strong exposure to e-commerce remain optimistic about growth prospects in 2026, while others are taking a more cautious, wait-and-see stance.

Even before the Middle East conflict escalated, indicators from some freight forwarders suggested they were less upbeat about 2026 and expected a downward pressure on rates as players chased market share, potentially pushing their sell rates to shippers lower.

Middle East

Demonstrating the volatility of international trade and how quickly the outlook picture can pivot, the outlook for air cargo now depends on the length and outcome of conflict in the Middle East.

Military strikes on Iran by the US and Israel, which commenced on 28 February, and Iran’s retaliatory response of targeting its neighbours in the region, brought Middle East commercial airspace to a virtual standstill. Airspace closures and flight cancellations withdrew 12% of global air cargo capacity from the market immediately.

Major regional hubs – such as Doha, Dubai, and Abu Dhabi – temporarily suspended flight operations amid multiple airspace restrictions, causing an immediate impact on the Asia–Europe air cargo corridor. The revenue impact of disrupted flight timetables is just one of the concerns for airlines. Jet fuel, a major airline cost component, could also rise materially if crude prices continue to climb. Industry analysts already report Brent crude oil prices above $80 per barrel, and these could potentially exceed $100 if oil production infrastructure is targeted due to tensions in the region.

If the conflict is brief and flights to/from the Middle East resume quickly, markets will normalise faster and reduce concerns of a longer-term spike in oil prices, but protracted disruption lasting weeks is likely to mean prices on affected markets could double or even triple.

A further escalation of the conflict could trigger a global energy shock and stagflationary pressures reminiscent of the 1970s, with sharply higher oil prices and a significant correction in equity markets, both unwelcome developments in relation to trade volumes, shipping costs, and retail prices.

Security fears for shipping using The Strait of Hormuz, which accounts for roughly 20% of global oil shipments and about 30% of global seaborne oil trade, have already been heightened with attacks on vessels in waters off the Persian Gulf.

Carriers will need to reroute freighters via Central Asia for technical stops or deploy more direct Asia–Europe services, depending on traffic rights, airspace availability, and operational constraints. This situation reduces the flexibility shippers previously relied on during Red Sea disruptions. When Houthi-related risks disrupted ocean routes, some volumes shifted from ocean to air; this time, that option may be more limited. Ocean carriers such as MSC and Maersk, which had previously signalled a return to the Red Sea, have now suspended Suez routings and reverted to round-Africa diversions.

So long as airlines can resume normal operations to, from and over the Middle East region, disruptions to ocean carriers may, once again, rescue air cargo demand and see upward pressure on air freight rates across Asia, Europe, and the Middle East. Rate increases would be driven primarily by capacity constraints and the speed at which carriers can reallocate lift away from the conflict zone.

Reset

On 21 February, the main talking point for the month was expected to be the US Supreme Court’s ruling to strike down the Trump administration’s broad ‘emergency’ tariffs, the subsequent introduction of temporary 10% tariffs, what it would mean for countries such as China and India, and the outlook for air cargo.

Then, on 28 February, came the strikes on Iran and the start of everything that has happened since. “This is the world we are living in, and the reality for businesses facing one new challenge after another,” said Niall van de Wouw, Xeneta’s chief airfreight officer.

“If we only had February’s data to focus on, we would say the start of the year has been encouraging for the air cargo market. Now, the stakes are raised.

“Past reactions to previous macro-events show that the global airfreight industry is highly skilled in finding creating solutions. But it will come at the price of higher logistical costs for the owner of the goods. But I am sure they will temporarily have no issue with paying such additional fees as long as they can serve their customers on time. In the coming weeks, we might see (again) the vulnerability and strength of the airfreight industry in the spotlight,” he added.