The impact of air cargo’s ‘black swan’ event – the conflict in the Red Sea that has disrupted shipping – showed signs of easing in April but volume growth still registered the fourth straight month of +11% increases in global air freight demand, according to the latest weekly data analysis by Xeneta.

Alongside easing in global air freight demand, the injection of extra cargo capacity as airlines launched their summer schedules boosted supply by +5% year-on-year in April. This put downward pressure on the dynamic load factor, which dropped from 62% in March to 59% in April.

Dynamic load factor is Xeneta’s measurement of cargo capacity utilisation based on volume and weight of cargo flown alongside capacity available.

In April, year-on-year growth in the global air cargo spot rate turned positive for the first time since August 2022, rising +5% due to a combination of Middle East conflicts and strong e-commerce demand. As a result, the average global spot rate rose to US$2.59 per kg, its highest level this year. However, this year-on-year growth in global spot rate should be viewed in the context of a weak market in April 2023.

“In absolute terms, the levels of demand and supply growth are what we expect to see in April after what was a typically strong month of March at the end of Q1. April may well represent an interlude to a quieter period for the air freight market,” said Xeneta chief airfreight officer, Niall van de Wouw.

He continued: “The growth in the spot rate was very much driven by regional developments as well as a case of market sentiment tending to follow market fundamentals. This is what happens in jumpy market conditions. The freight rate in April was a reaction to high first quarter volumes, but we expect rates to ease.”

Shippers and forwarders coming to terms with delays in ocean freight services due to diversions from the Red Sea will also have an impact on air cargo demand, according to van de Wouw: “We have clearly seen a push for airfreight capacity around the Indian subcontinent because of the Red Sea disruption, but this impact is easing as businesses which depend on ocean freight are now planning in longer lead times. So, we expect the recent surge in demand for airfreight in this region to lessen.”

Xeneta began to see a downward trend in air freight spot rates emerging in the third week of April from this region.

The China to US market led in terms of freight rate growth in April, jumping +20% month-on-month to $4.87 per kg. This was followed by outbound freight from the Middle East and Central Asia region. In April, average spot rates to Europe and the US grew at a similar rate of +18% month-on-month, reaching $3.29 per kg and $4.79 per kg respectively.

The outbound Southeast Asia market followed suit as it is highly sensitive to events in nearby regions. The Southeast Asia to Europe spot rate in April rose by +14% month-on-month in April to $3.06 per kg, while the rate to the US increased +12% to $4.66 per kg.

Conversely, the only major region to see a significant decline in freight rate was the Europe to US market, with the April spot rate falling -8% month-on-month to $1.93 per kg.

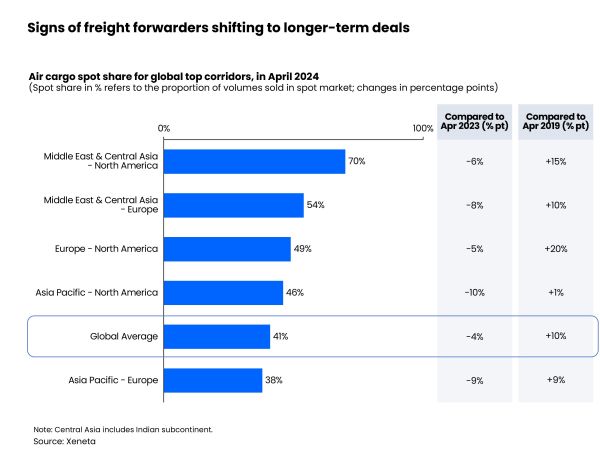

The Asia Pacific to North America market experienced the largest spot share decline in April at -10% pts compared to a year ago, shrinking its gap with the pre-pandemic level to just +1% pt. Xeneta’s spot rate share refers to the proportion of cargo volumes sold in the spot market.

In contrast, the Europe to North America market only saw a modest spot share decline of -5% pts. Its spot rate remained +20% pts above the pre-pandemic level for the same period. This reflects the market expectation of milder freight rate adjustments for the transatlantic market thanks to adequate cargo capacity and freight rate levels getting closer to their pre-pandemic levels.

April typically marks the beginning of the traditional slack season for the global air cargo market. A slowdown in global cargo demand growth became apparent in the air freight rate trend in the final weeks of April.

Xeneta also saw more freight buyers shifting away from the spot market, in which freight rates are valid for up to one month. In April, the global spot share averaged 41%, down 4% pts from a year earlier. However, it remained +10% pts above the pre-pandemic level for the same period.

Attention is now turning to the fourth quarter as shippers and forwarders make an early start to their peak season planning after the market experience of 2023.

Van de Wouw said: “There’s the reality of now, where you will see load factor decline on markets because of the increase in capacity, sitting alongside the preparations already under way for Q4. That’s top of mind for shippers, forwarders and, to a lesser extent, airlines, and they are jockeying for position after a ‘strong’ peak season last year.

“Before then, there was no prior experience of the order of magnitude of the e-commerce behemoths and their impact on air cargo’s traditional peak season market. This year, the traditional market is looking to de-risk and will plan to be better prepared.

“Q4 is just around the corner in planning terms and freight forwarders are already looking beyond the summer to secure market share because they are concerned about what e-commerce is going to do out of southern China and Hong Kong later in the year.”

One surprise, van de Wouw adds, is the price validity periods of new contracts between shippers and forwarders. “We see a big swing from agreements increasing in length to a reversed trend of more short-term contracts as shippers look to buy a bit of time because of the black swan event in the Red Sea. We also see more agreements between shippers and forwarders which contain a mechanism to deal with market rate changes throughout the validity of their contracts. This reflects how the need to manage market volatility is surpassing the typical wheeling and dealing over the last few cents in contracts.

“Shippers will prefer longer-lasting relationships with freight forwarders that know their business, delivering good operational performance at a competitive rate level. Freight forwarders want predictability of their revenues to avoid having to go to tender each quarter to secure the business. So, these mechanisms can work for both parties,” he said.

But, while forwarders are looking to buy more longer-term capacity, airlines face ‘a balancing act’. Van de Wouw added: “If airlines think Q4 is going to be busy again, they’re not going to sell all their capacity now. They must decide how much they want to commit now, knowing they can possibly get up to 50% more revenue for that same capacity on the short-term market in Q4.”