Longer-term contracts between shippers and freight forwarders may signal ‘more common ground’ in a stabilising global air cargo market says industry analysts CLIVE Data Services, part of Xeneta.

In its report published on 5 April, it said that demand dipped by -3% year-over-year in March.

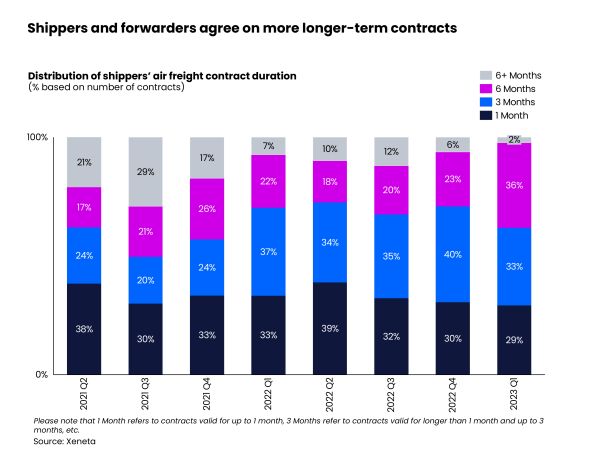

The number of six-month shippers’ agreements rose to 36% versus 23% in the fourth quarter of 2022, a shift which Xeneta chief airfreight officer Niall van de Wouw, said could indicate a “hunt for volume” by forwarders wanting to lock-in customers for longer.

Meanwhile, some retailers are getting concerned about the hoped for rise in consumer spending in the third quarter of this year and a resulting need to restock inventory levels. As the cost-of-living crisis gather pace in prime consumer markets, and the conflict in Ukraine shows no sign of abating, retailers now fear a slower and subdued market, meaning restocking and the peak season airfreight windfall this usually creates may not materialise.

Niall van de Wouw said: “I think we’re seeing signs that some forwarders are willing to take a little more risk on what airfreight rates might do because they don’t expect the market to drop much further. Everybody wants to achieve growth, but if the market is not growing, you have to grab a share from someone else.

“The fact that we see longer term contracts between shippers and freight forwarders is a signal that the market is stabilising. Shippers have regained some ground because of the lower rate conditions, which have affected the airlines and forwarders, but it’s not like the bloodbath we see in the ocean market.”

The global airfreight market continued to normalize in March. The -38% reduction in the general air freight spot rate year-on-year produced an average rate cost of US$2.62 per kg, a -4% decline over February. This is attributed to both shrinking cargo volumes and recovering cargo capacity. Global cargo volumes have been falling for the past 13 consecutive months but showed some sign of relief in March, as volumes registered their smallest drop of -3% year-over-year, the lowest monthly decline in over a year.

International cargo capacity continued to recover in March, recording its largest increase of 16% from a year earlier. CLIVE’s global dynamic load factor in March was 60%, 6% pts adrift of the same month a year earlier but recovered 6% pts from the seasonal low in January this year.

March 2023 data must also be considered against the market impact created by Russia’s invasion of Ukraine, which began just over 12 months ago.

Among the world’s top three corridors, the previously resilient transatlantic westbound air cargo trade registered its first year-on-year volume fall of -11% in March. This was in line with the latest German and UK manufacturing Purchasing Managers Index, which both indicated shrinking manufacturing activities.

The average general airfreight spot rate from Europe to the US in March fell -46% versus March 2022 to US$2.71 per kg. It was the only corridor among the world’s top three to record a year-end freight rate increase last year.

The market is yet to see any meaningful impact on air freight rates resulting from recent strikes in some European airports. Germany, France, Spain, and the UK were the latest countries to face disruption caused by airport strikes, threatening supply chain disturbances. Further industrial action is due in France and the UK over the Easter break.

In contrast to the transatlantic corridor, the outbound China cargo market bounced back compared to global market downturns. Supported by upbeat Chinese manufacturing activities, with its PMI readings showing expansion for two months in-a-row, March volumes out of mainland China grew 30% from last month and were down only -2% from a year earlier. But the growth of air cargo capacity outpaced the growth of volumes. For instance, the capacity from mainland China to Europe restored 63% month-over-month and 155% from a year ago in March.

Air freight spot rates from mainland China to the US and Europe stood at US$5.07 per kg and US$3.65 per kg respectively in March, both down -7% month-over-month and -43% from a year earlier. But it is worth noting that for both corridors the downward pressure on rates started to ease from the second week of March, with rates stabilizing until the month end.

Looking ahead, Hong Kong is expected to receive a boost as the government eases a ban on transshipments of e-cigarettes and vapes products via Hong Kong. The restriction, which was imposed in April last year, cut cargo volumes equivalent to 10% of Hong Kong’s annual export volumes.

In the face of global economic headwinds, the jet fuel price remains highly volatile. The aviation market expects higher jet fuel costs as crude oil prices soared after last week’s announcement of production cuts from OPEC+, a group of the world’s largest oil producers.

Niall van de Wouw commented: “We don’t see an air freight market in crisis, we see it finding a new baseline, which we referenced last month when we acknowledged the need to move on from pre-Covid comparisons.

“If we are seeing a shift to longer-term contracts, this will certainly benefit shippers’ logistics purchasing departments which, due to the level of volatility in the industry, have been forced away from traditional annual deals. Their core business is making pills or smartphones, for example, and not about having to renegotiate air freight rates every week or every month.

“We see a calming down and a greater appetite for shippers and forwarders to come together on a longer term. There’s more common ground for longer-term deals in a positive way. The next interesting market development is what airlines do with their summer schedules and the further capacity boost this traditionally brings?”