Analyst Niall van de Wouw has described US President Trump’s ‘Liberation Day’ – in which he announced major tariff hikes on imports from most of the country’s trading partners as “a seismic shock” for e-commerce.

De Wouw, who is Xeneta’s chief airfreight officer, said that the cargo market is reevaluating its future as shippers, forwarders, airlines, and consumers come to terms with the economic reality of new import taxes and a potential international trade war.

As expected Trump has also confirmed the elimination of duty–free de minimis treatment for low-value imports from China and Hong Kong, starting 2 May. All relevant postal items valued at or under US$800 previously qualifying for the de minimis exemption will become subject to a duty rate of either 30% of their value or US$25 per item (increasing to US$50 per item after 1 June 2025).

The announcement was one of many as Trump imposed sweeping global import taxes on goods into the US from 9 April.

Already reeling from the potential impact of the US’ actions, global air cargo demand is likely to suffer further harm from retaliatory actions by other countries. EU President, Ursula von der Leyen, called the US decision “a major blow for the world economy.”

De Wouw warned that after more than a year of double-digit growth, air cargo now faces an uncertain future.

“In my 30 years working in the air freight industry, I cannot remember any other unilateral trade policy decision with the potential to have such a profound impact on the market at a global level,” he said.

“E-commerce has been the main driver behind air cargo demand. If you suddenly and dramatically remove the oxygen from that demand, it will cause a seismic shock to the market,” he added.

China-to-US e-commerce shipments alone account for roughly half of the cargo capacity on this eastbound corridor and around 6% of global air freight demand. Amy disruption to this will free up a significant part of this corridor’s cargo capacity and spread its impact to the rest of the market, van de Wouw said.

Air cargo market data for March clearly indicated shippers and forwarders were ‘hedging their bets’ and buying time before making longer-term commitments to capacity as they waited to see how the impact of newly-imposed tariffs and international trade tensions unfolded. In fact, there were no majorc signs of panic as demand rose +5% year-on-year against a strong comparison 12 months ago.

However, the economic fallout following the latest events is now likely to place further pressure on airfreight rates. Global air cargo spot rates in March continued their levelling out trend seen over the past year, increasing at their lowest pace since June 2024 at +6% year-on-year.

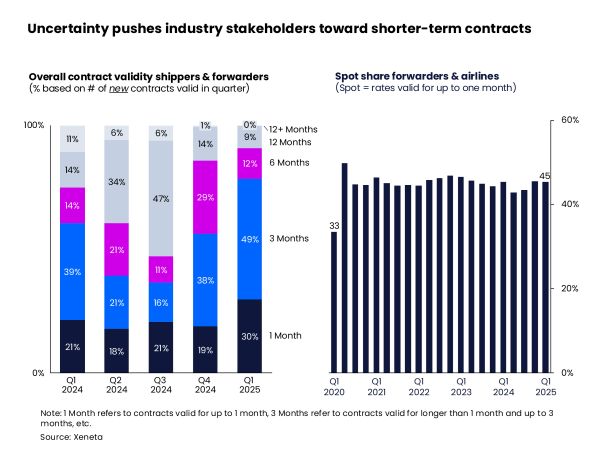

Given the tumultuous market uncertainties, the latest air cargo market data reflected the cautious ‘wait and see’ approach being adopted by industry stakeholders. Shippers negotiating contracts in Q1 2025 preferred shorter-term agreements of three months or less, representing 79% of contracts – an increase of nearly 20 percentage points year-on-year. Meanwhile, freight forwarders continue to place approximately 45% of their volumes in the spot market.

“With the growth of rates slowing overall, we’d normally expect to see shippers making longer capacity commitments to achieve more competitive rates, but, right now, this is clearly a gamble few shippers are ready to take – and this is before we’re even seeing tariffs impacting volumes,” said De Wouw.

He continued: “Considering the economic tensions between the US and its international trading partners, this hesitance is understandable and yesterday’s ‘Liberation Day’ statement by President Trump will take this to a level we haven’t seen before. As companies come to terms with the impact of US tariffs and we await the global response, shippers simply don’t yet know what they’re up against. If they agree a plan for the year now, it could turn out to be much costlier in the longer-term.”

It’s also a ‘big ask’ for a freight forwarder to commit to a fixed rate for a year, even with various ‘escape clauses’ in place, van de Wouw added. “In this environment, the T&Cs are becoming just as important as the air freight rate,” he said.

March saw a third consecutive month of tempered single-digit global air cargo demand growth, although not as subdued as might be expected. The temporary suspension of the de minimis ban by the US government on inbound Chinese shipments produced a recovery in transpacific e-commerce demand, but this is set to change following the latests announcement.

The impact on e-commerce volumes carried by air into the US will not only mean higher prices for consumers, it also raises the prospect of increased border congestion given the sudden and dramatic increase in shipments needing to be processed by US Customs and Border protection. The US Department of Commerce attempted to allay these concerns by stating it has adequate systems in place to collect additional tariff revenue on the 4 million de minimis shipments a day entering the US.

Global air cargo supply grew +2% year-on-year in March, but this was still at slower than demand growth. With a combination of supply/demand rebalancing, the dynamic load factor stayed on par with last year at 60%.

The addition of summer capacity from the end of March to satisfy peak passenger travel demand could see one of two scenarios unfolding in the current climate, van de Wouw indicated.

“There appears to be a fundamental shift in sentiment emerging in the consumer market in response to the potential chaos and added costs of tariffs being imposed on and by countries and trading blocs.What happens if there is less passenger demand across the Atlantic this summer? Less passengers means less bags, which produces even more cargo capacity in the market. If passenger and cargo volumes feel an impact, the next step might be for airlines to downgrade or divert capacity.”

In terms of regional developments, despite double-digit demand growth month-on-month in March, Northeast Asia to Europe spot rates were unchanged at US$4.28 per kg as airlines allocated more capacity to the market. Thanks to buoyant e-commerce demand during the month, the corridor’s spot rate increased +14% year-on-year. In contrast, the trade imbalance meant backhaul trade showed a -2% rate decline month-on-month and -14% year-on-year to $1.37 per kg.

The Northeast Asia to North America market showed a noticeable spot rate increase of +9% month-on-month to $4.17 per kg, undoubtedly driven by the temporary removal of the de minims threshold for Chinese shipments in early February.

Similar to the Europe to Northeast Asia corridor, the North America to Northeast Asia market showed a slight decline of -1% month-on-month and a considerable -20% spot rate reduction year-on-year.

Unusually, the Transatlantic market recorded both fronthaul and backhaul rates increases in March. The westbound air spot rate grew +2% month-on-month to $2.51 per kg and +22% year-on-year. Eastbound rates grew +4% month-on-month and were +1% higher year-on-year to $1.11 per kg.

Niall van de Wouw says market anxiety and uncertainty is not good for anyone: producers, consumers, airlines, or forwarders. “It’s a crazy environment, left and right,” he said.

“No one is benefitting from this situation because it’s impossible to plan effectively against a moving target. Clearly, everyone will be waiting to see how the removal of the de minimis threshold and all the global tariffs already announced and those still to come will impact trade, as well as how quickly there will be less demand and, consequently, less airfreight. It’s all expectations right now, but we must expect the situation will get worse before it gets better.”